Luxury accomodation on the warm indian ocean, going so cheaply you wouldn’t believe it. Come view now… in Mogadishu!

I’ve written before about how I’m really not a fan of a buy to let property as an investment, but what about a buy to live in property? Luckily for you, I’ve done that before too. In the last property article I mentioned the house with a built-in hole in the back yard for pouring cash into. Well now having just sold the property I can provide some real numbers to answer that question.

The numbers:

Purchase date: 2010-02-19

Purchase price: R1 260 000

Selling date: 2015-02-19

Date of transfer (estimated): 2015-05-01

Selling price: R1 320 000

Total profit on sale: R60 000

Less Transfer costs on purchase: R34 000

Less bond cancellation fee: R3 000

Less agents commission @ 5%+VAT: R75 240

Less maintenance on the property over 5 years: R120 000

Net gain: -R142 540, over 5 years on an investment of R1 294 000.

Yes, I lost money on my house. Plenty of it. As an investment, it offered returns of -3% annualised over five years. Pass me a kleenex.

Now of course you’re saying that I didn’t really lose that much because I had a roof over my head, but let’s see if you still feel that way after the following mental mathematics.

Would I have spent more if I’d rented?

Rent in 2010 for the same property would have been R7000, but the renter wouldn’t have had to pay levy or rates and taxes like the owner, so I’ll take that off the total rent. In that case, the 2010 rent would have been R5900 (Rates were about R500, levy started off at R600, both increased pretty much in line with inflation).

That means that over 5 years, increasing rent at just 6% a year, a tenant would have spent R399 106 in rent for that exact property. On first glance it looks like the renter would have paid an extra R256 566 (R399 106-R142 540) compared to the homeowner.

But as with all these articles, the bottom line is never really the bottom line. After all, we’re super shrewd savers and investors on this site, not your average Joe Schmo big spender. With that in mind, let’s see what would have happened if I’d invested the money instead. An initial sum of R1 294 000, price plus transfer fees, over a 5 year period. As the 5 year period ends now, I can simply load the Satrix website (Note: Satrix has never paid me for any of these plugs, though I really think they should!) up and plug in the numbers.

Initial investment: R1,294,000

Total investment value after 5 years: R4,469,634.74

Growth on investment (dividends reinvested): R3,175,634.74

Performance per annum (dividends reinvested): 28.13%

Absolute performance (dividends reinvested on payment date): 245.41%

Hmm, so if I take my profit, and then take off R399 106 for my rent payments, I’m still sitting on an extra R2 776 000 in cash after the 5 year period. Time to put away the kleenex and search for LifeLine’s number.

If I add that value to my current portfolio it makes me a rich man! Those figures are for the Satrix Indi, which produced a scorching 28.13% p.a. over the last 5 year period, so the fine print of past results not being an indicator of future results yada yada applies as usual.

That is of course buying the house cash. What about the average person who put down a 10% deposit and made monthly bond payments?

Bond repayment numbers

Initial investment: R129 400

Monthly bond payment @ prime -1.5%: R11 750

Less the net rent that would have been paid: R5 850

Plus the average monthly maintenance paid as an owner: R2 000

Total invest-able amount: R7 900

Total profit from renting and investing the difference for 5 years: R1 485 758,2

So on to the moral of the story.

If you’re trying to decide between buying a house with a bond or renting a similar house, rent the damn thing!

If you’re trying to decide between buying a house cash or renting a similar house, go speak to your psychiatrist, clearly your medication isn’t strong enough.

Not only is a house a bad investment, it also reduces your flexibility:

- Your likelihood of moving to a new city for a better investment will be far lower if you’re a homeowner rather than a renter.

- If your neighborhood goes to the dogs, you would be tied to it, and to a sinking asset unless you cut your losses and tried to sell.

- Your wife falls pregnant with triplets and you need a bigger house… Well then I hope you have a decent stash of cash for diapers, but also because switching houses costs a fortune in time and money.

- Government goes berserk and makes you want to leave the country. Sorry your now rapidly reducing asset is going to try keep you here.

- Interest rates go through the roof. Suck it up and keep on paying. Ditto for property taxes.

Now since Mr Malema has asked us to “hand over some of our property“, he clearly has our financial well being at heart. Just make sure you take it with the bond, burnt out pool pump, and don’t forget the wonderful rising damp! Where can I send the thank you card?

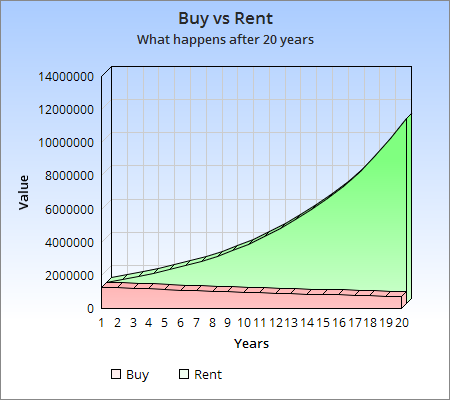

Buying vs renting after 20 years

*Caveat: The main reason I spent so much on maintenance for this house, was because it was built in an area with fairly bad damp. Well damp and the stupid pool. The damp and the cost of HTH, pool pump repairs, electricity for the pool pump is enough to make me feel ill. Worse syill, on selling, a professional damp inspector noted another R80 000 worth of work needed. Of course the consumer protection act means you can’t hide this fact, and therefore my offers were all pretty much reduced by that amount.

*Another caveat: Just like the last time, South African’s are really lousy savers. Having a bond almost forces them to save the value of the house over a 20 years period. I think on average it’s a good thing, but if you’re already saving money, there are far better places to put it than on a second property. And like I’ve said before, if you want to buy a house, buy it. Not because it’ll be a good investment, but because it’s a place you see yourself wanting to live, and a place for your kids to grow up in.