It’s budget reconciliation time

For far too long I’ve been spending with wanton abandon and not even caring enough to add up the numbers. How could I be setting such a terrible example to all the millions of readers who don’t make their way to my blog. This is going to to change. Starting from now there will be an annual post where I air the dirty laundry of my multitude of credit card receipts.

So now to go and break tradition with seemingly every other blog post I read lately, I’ll actually get straight to the point and just pop the numbers out. None of this read my life story before you get to the delicious recipe, or navigate past all the annoying subscription popups before I actually get to see a number on the page. No, just no!

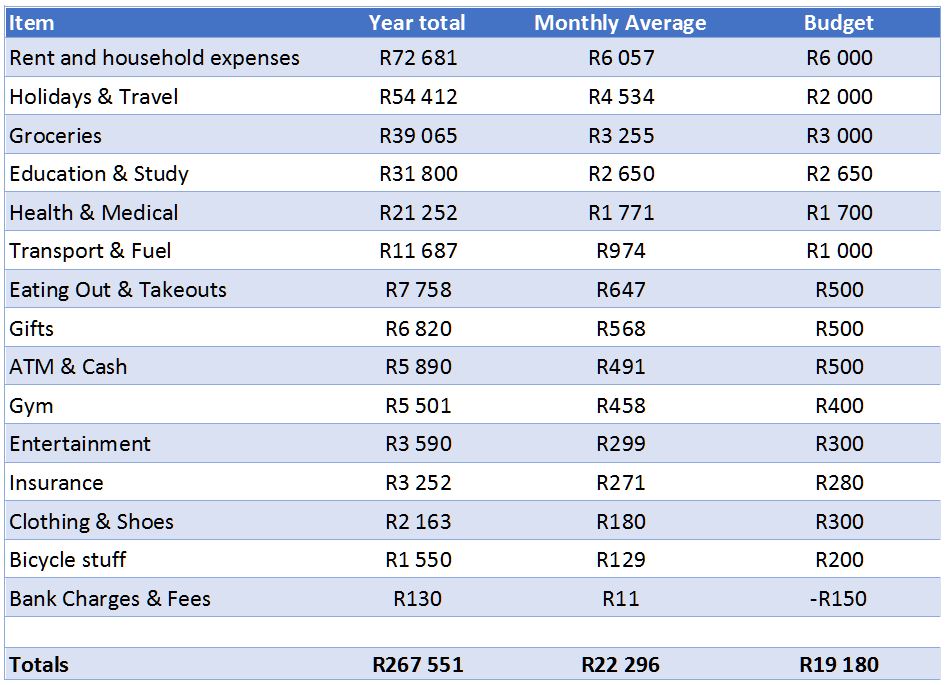

My spending is right here:

Buckle up, it’s been a big year!

Still with me? Okay then I’ll get into a few stories.

Rent

We must be idiots. We spend the majority of our money just so we can sleep inside a glorified prison cell with a view that never changes, and bills that never stop coming. Well when I say we I mean people who can say no to million dollar cars and rather drive jap econo boxes, otherwise like many South Africans, they probably spend more on their car than a place to live.

I’m quite happy to personally not own any of these miserable excuses for investments that have in real currency terms actually decreased in value every year since 2007, with a small exception in the Republic of the Atlantic Seaboard. My wife though does, but she got lucky. She bought before the boom in an unpopular area that was walking distance to the office, and has now become quite popular.

Since getting married, we decided she can keep her walking commute as I have a fantastic bicycle to get to work on, making me her tenant. For a place to live I think I get quite a good deal. It’s a beautiful apartment, with space to park my car and bicycles. I have two friendly dogs to play with, not too much of a challenge to get to work, and I get to sleep with the landlord. But it’s still by far my biggest monthly expense.

In future I plan to beat the system. I’ll be going totally nomadic where I actually have some control over what my living costs will be. Depending on when I actually pull the plug, and how good a negotiator I am, that could be a camper-van, small sailboat or luxury catamaran.

Holidays

Where am I? Hard to believe, but this is Rome.

I’m very lucky because I get to travel for work quite a lot. Almost exclusively overseas, though usually to places most South Africans don’t pencil onto their bucket lists.

Last year was one of the quieter years for me, but I still had business trips to Kenya, Switzerland, Mozambique (twice), Italy and the Republic of Congo. Oh and I also had one to Cape Town which is my favourite local destination.

You’d imagine that someone who has to travel that much for his job would just want to stay in SA for his holidays but no, I had to add another 5 countries to that list: Chile, Argentina, England, Germany and Portugal. You know because five countries in a year would be so inferior on the imaginary Jones’ travel scorecard.

Of course I had fantastically good reasons for traveling, and they were all once in a lifetime opportunities as they always are, but in total I blew through over R54 000 on foreign trips, more than R30 000 higher than I budget for. If you’re keen to read more on the trips head on over to my death spiral blog post and to the 2017 lessons learnt post. You can also find a bunch of pictures on our travel instagram.

Groceries

Yes I spend a lot on groceries, it’s Tim Noakes’ fault. Actually not because I was banting for years before he told me it was called banting. Happily though he’s made it easy to get actually edible bread and convenient microwave meals that won’t add inches to my waistline. I’m sure he’s also the reason that I now have to pay R25 for an avo, madness!

Education

I’m quite lucky that my son goes to the best government primary school in Johannesburg according to some voting criteria I know nothing about. But I must agree, as government schools go they really seem to have their act together, and the fees are pretty good too. The total above even includes the optional R9600 per year for aftercare.

Health

This isn’t an area you can really skimp on. When the kid or wife is sick, they go to the doctor. When the husband is sick he comes up with reasons why he doesn’t need the doctor and gets into trouble with wife. We have an international medical insurance through my job, so this total includes my R1040 premium share as well as the 20% share we have to pay for doctors and medicines. There’s also a few trips to Clicks and Dischem bundled in here.

Transport

I love my car. It never lets me down, and feels like a faithful golden retriever. Sure it’s not that fast, and looks a little scruffy, but it’s my friend. Happily I often do more than 900km on a tank, with a few liters to spare, and when it comes time to service I don’t need to prep with vaseline when making the payment. The total costs here include a few Uber trips too, usually when on holiday.

Eating out and takeouts

I overdid this towards the end of last year. There are more than a few convenience meal purchases, and far too many trips to Andiccios for the best cauliflower base pizza north of the Vaal. I will be stronger in 2018 I promise. Well maybe from tomorrow, apparently her sexiness is bringing home pizza this evening, and I didn’t even half try to argue.

Gifts

Don’t say I’m not generous. Ignore what everyone says, when someone invites you to a wedding, they’d like to be able to fold the gift inside their wallet. It’s almost like a direct money transfer from the father of the bride to the guy who’s sleeping with his daughter, and you’re the proxy making it happen.

I had one wedding gift, a few gifts for the lady of the house, and of course for the boy who’s now 11. That meant he also got his first bank account, which I kindly stocked with a handful of notes. It’s with Capitec too, so he’s loving his first taste of compound interest. I also tried spoiling myself with a birthday present at the end of last year, but since it seems the post office has “lost” it, I might have to get a refund.

Cash

All the financial gurus will tell you that you shouldn’t use credit cards so you can feel yourself spending money, and they’re all wrong. Cash is just an easy way to hide the fact that you’ve got an Starbucks latte problem or that you’ve spent a fortune on hookers and cocaine. It’s time to patch together that cut up credit card and instead shred your cash. Not literally of course, and a debit card makes a very safe substitute for a credit card.

The key here is accountability. If I only spent cash there’s not a hope in hell I’d be able to tally up my spending numbers, and I’m willing to bet it’s the same case for you.

Gym

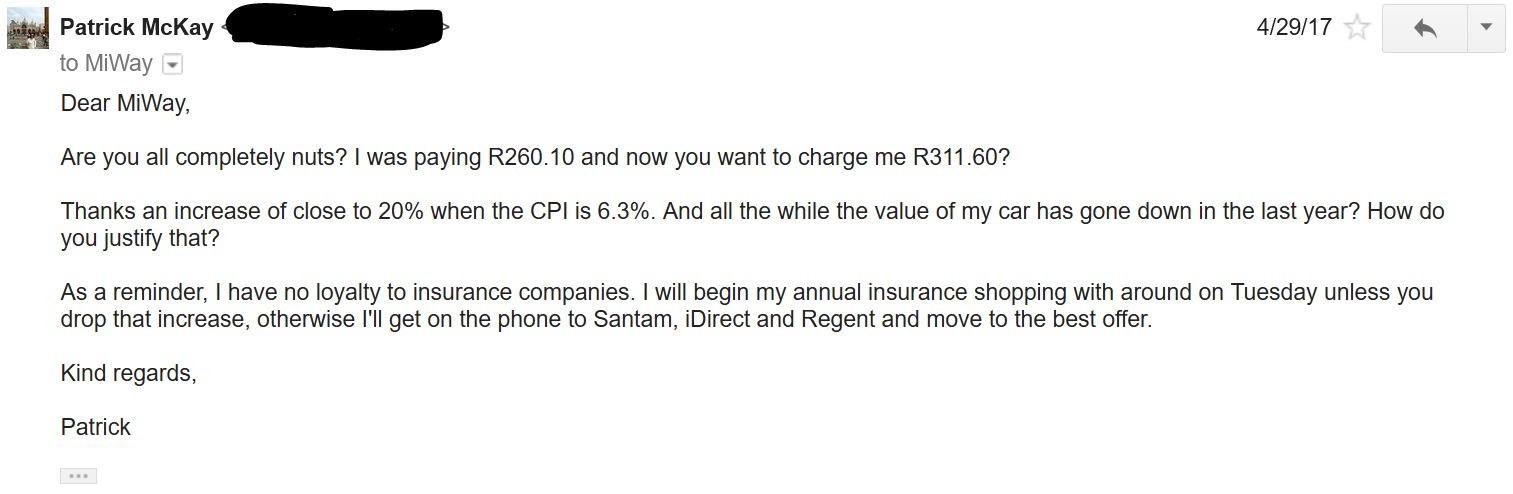

I suppose this could have come under the health section, but it’s possible to stay healthy without the gym. I upgraded to a multi club membership briefly last year, found out it was a mistake and then downgraded again. I also had a huge twitter fight with Virgin Active who thought they could up the prices as they felt like. I won.

Entertainment

When I was in London a truly astoundingly large group of ex-South Africans invited me to watch the sevens rugby at Twickenham. Even though I’m not a rugby fan it was tons of fun and great catching up with everyone. My son loves going to the fun company, mainly to challenge the arm wrestling machine, so we went a few times. He also seems to like winning tickets so he can use them to buy weird Chinese toys. I’ve told him often that it would be far better value for money if I just bought him those with cash, but he disagreed.

There are also a few trips to the planetarium which I think is probably the best value for money kids outing in Joburg. If anyone can think of a way a dad and child can have more fun for under R85 please let me know. Aside from that we went to the zoo a couple of times, and also to the movies every now and then.

Insurance

They gave me a 6% increase

Clothing and shoes

I’m not big into clothes. I try to run a one in one out policy with the things I wear, and the one out is usually worn out. I have a growing boy though, so he needs new shoes or soccer boots at least once a year. School clothes too, but thanks to that Steinhoff subsidiary Pep they’re actually quite cheap.

Bicycle stuff

Last year I serviced my front fork which was rather pricy, and as usual I went through plenty of brake pads. This category has gotten of to a bad start in 2018, as after 18000+ perfect kilometers my electric bike has developed an annoying judder on pull off. It’s either the motor which is hopefully repairable, or the controller which is replaceable. Both will cost me a couple of thousand I’m imagining, but I’ll make that back after under 1000km of use.

Bank Charges

Like I said in the last post, I found a way to get negative bank fees through a combination of Capitec and Virgin Money. Now all I have to do is hope that Viceroy is wrong and that Capitec continues to be the great bank I’m finding them to be.

Update: Investments

One of the forum members Graham pointed out in the comments that I don’t have any investments listed here. That’s because I don’t consider investments to be spending. I did put R33 000 into both my and my sons tax free savings accounts. He’s loving watching it grow, with it sitting on over R100 000 already! The rest of my investments went offshore into the Vanguard FTSE All-World UCITS ETF as discussed in this blog post.

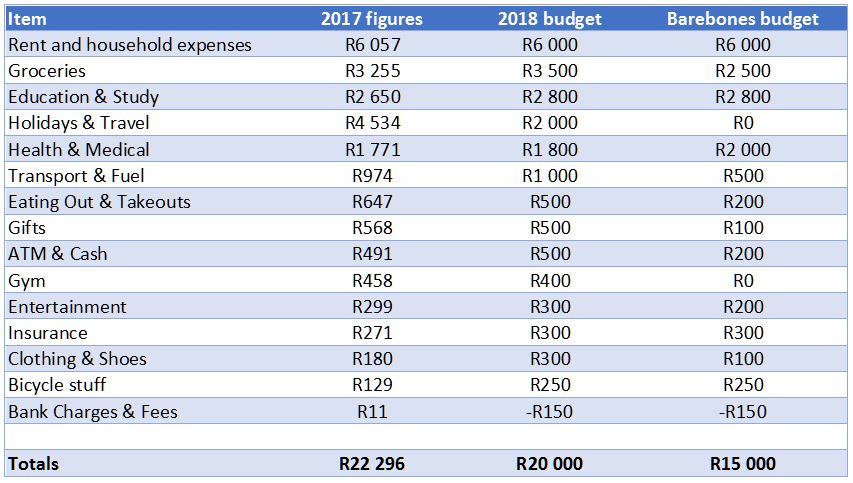

2018 budget

I’m going to try and trim my spending back by around 10% in 2018 to see if I can keep it to R20k or less. Also since hearing all the horror stories from the many colleagues who are soon to be out of work, I’ve tried to estimate what my barebones budget would be just in case my job vanished and my side income dried up completely.

Here’s my thinking on the barebones budget. There’s not much I can do about rent now, so that has to stay. I could definitely cut back on groceries by removing luxuries and substituting for cheaper options, eggs vs meat etc. My dividends and sideline income covers my budget, but this is a worst case scenario where the sideline income goes too, so no more holidays for me.

Here’s my thinking on the barebones budget. There’s not much I can do about rent now, so that has to stay. I could definitely cut back on groceries by removing luxuries and substituting for cheaper options, eggs vs meat etc. My dividends and sideline income covers my budget, but this is a worst case scenario where the sideline income goes too, so no more holidays for me.

Medical would go up, I’d take the cheapest hospital plan for my son and I, my wife would need to pay for her own, sorry hon. I’d cut my driving in half, instead using my free time to cycle nearly everywhere. That would be great exercise, and by adding in some bodyweight type exercises I could lose the gym membership.

Without needing to work I’d cut way back on clothing. I have plenty casual clothes to last me for ages. Kid still has many years to grow though. I could cut aftercare, but at just R800 a month it would free up a lot of time for trying to find ways to get some more money in.

Do you have any great spending tricks to help save money? Use the comments section below to let me know.