Dear Investor Challenge,

I’d like to get rich, how do I do that?

Thanks,

I.M. Gettingby

Einstein apparently said this

Well this is a pleasant change Mr Gettingby. The last guy to write in was trying to lose money. Tough nut to crack that one is. What you want is soooo much easier to achieve. Well yes, of course I can help. It’s really simple in fact. Here’s the only way to get rich in one sentence:

Spend less than you earn, and invest the rest.

The end.

Short blog wasn’t it. I put in almost as much effort into the answer as you did in your letter. I guess you didn’t get your money’s worth out of this post. Wait I think I hear the sound of Oliver Twist “Please sir can I have some more?”. Luckily for you I’m far kinder than the orphanage keeper, so yes, you can in fact have some more.

First off, we need to define rich. As all people are different, there’s no real universal definition. An article on yahoo finance looked at this a while back. They quote a study showing that older people defined getting rich as having security, while younger people said it meant having more fun. We can also look at some practical examples. Many would consider Mike Tyson a rich man in the peak of his career, and they should have been right. Over his career he earned more than $400 million, but he was spending a far higher percentage of his income than he should have been. Because of this, it comes as no surprise that in 2004 he was $38 million in debt!

In contrast, I took a few months off work to be a paragliding bum in Cape Town (I’ll tell you more about the benefits of having FU money later. Edit, I can tell you about it now), and there was one guy who was on the mountain just about every flyable day. He didn’t have an expensive car, or dress very smartly, but from speaking to him I found out that he didn’t really have to work, he owned a fleet of classic cars he use to rent out to people in the movie and advertising business, and he was free to spend his time doing whatever he felt like. These examples tie in quite well with the way Warren Buffett describes wealth, as having enough “To allow me to do what I want to do everyday”. I like that, so now I’ll be using it. Feel free to send me an invoice for royalties Warren.

Now that we know what being rich is, all we have to do is get there. Firstly stop arguing. Aside from spending far less than you earn and investing the rest, there’s no other way you’ll get rich. You’re not going to win the lottery, I promise, and don’t try to tell me you’ll be a pro footballer. Even if you are, you’ll only be rich if you spend less than you earn, and I already told you that. Marry rich maybe? NO! You should never marry for money… rather divorce for it 😉

Okay, so we have one practical method for getting rich, now there are two questions:

1) How much less than my net salary can I spend, and

2) What should I do with the rest?

Well maybe he didn’t…

Let’s start with question 2, the easier question to answer, what should I do with the money I don’t spend? Well, unless you know classic cars inside out like the guy I was speaking about (and even though your BMW or Audi will cost you a million dollars, it’s not a classic!), or you’re an expert on the property market, and don’t mind being a landlord, or you have some other skill or talent that will give you a REAL edge over everyone else in a particular field, you should just buy into diversified index funds (Exchange Traded Funds), without trying to time the market, or heaven forbid, beat it. I’ve already shown you why. So collect those index funds, over time, nothing will beat them. Property may have briefly in booms, gold has had moments too, but since you wouldn’t know when to buy gold or when to sell, you’d be wasting your money and forcing yourself to spend less time doing what you want to do every day. Don’t do anything else, just keep sticking cash into the indexes.

Sorted. Now you know where to put your cash, let’s move back to the first question. How much of your cash do you need to stash?

First, some assumptions. Since everyone is different, we’ll assume that you want to spend as much while doing what you want to do, as you currently spend doing what the boss says you have to do. None of this live off 70% of my final paycheck nonsense the advisers keep telling me about. Actually they’re right. Most people spend less after retiring. Sadly for most, it’s because they haven’t stashed quite enough away. On the plus side, work related expenses generally do drop after retirement (no more suits or the daily commute!). But for us, we’re not going to sit around feeling old and shouting at the noisy kids next door, while eating polony on toast. We’d like to keep doing cool stuff. After all, we would ideally like to be rich before we need dentures and plastic hips.

The second assumption is how much of your total stash you can spend every year without having to worry about selling any kidneys at some point in the future, or having to marry a Gupta. Fortunately a bunch of smart guys at Coronation fund managers have done the heavy brainwork here, and it turns out that South Africa has a 100% guaranteed safe maximum (imaginatively named SAFEMAX) of 3.84%. This means that if you had gone on retirement any time in the past 110 years and drawn 3.84% of your capital per year you would have been just fine. This is a very similar number to a large number of first world countries with the US, UK, Australia, Switzerland, Denmark and Sweden all ending up with a SAFEMAX from 3.6% to 4.4%.

To make life easier for future calculations I’m going to just say that 4% is the safe draw-down rate. Most financial advisers in SA seem to quote 6%. One fairly well known web personality quotes 8%, but I think she’s being overly optimistic. A 5% rate gives you 90% chance of not running into trouble, and I personally wouldn’t like to risk my future on anything less than a 90% success rate. The 4% rate should succeed at least 98% of the time.

Okay, now that we know how much of our stash we can use every year, there’s a quick and easy formula to work out how much you need to have stashed to be rich. All you need to do is take your monthly expenses and multiply them by 300. Scary number isn’t it! If you’re like most people, you probably spend all of your salary. If you’re unlucky, even more than that thanks to those wonderful plastic rectangles in your wallet. It doesn’t take a genius to realise that you’ll probably never have a stash of cash (err stocks) big enough to do what you want to do every day. But don’t worry. The wonderful thing about investing is that your stash grows its own stash. Really quickly even. In fact after a few years, your stash will be growing more stash far faster than you can add to it. This wonderful concept is known as compound interest. Einstein reportedly called compounding “the most powerful force in the universe”.

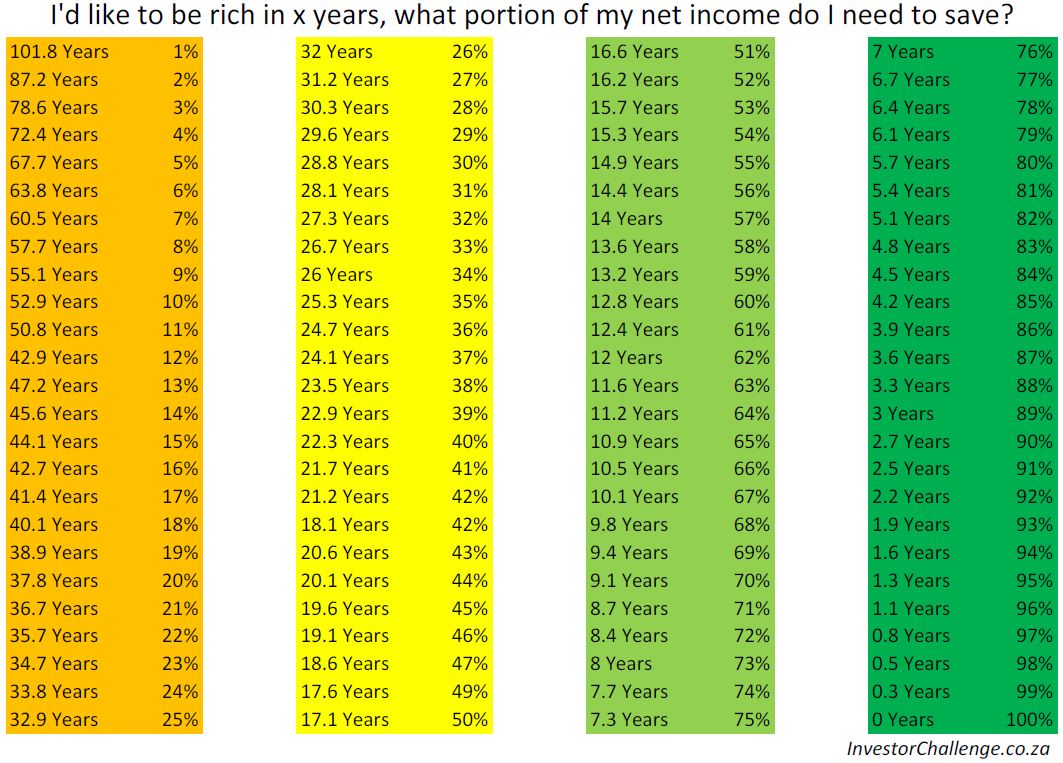

All you need to do now, is decide how long you’d like to take to be rich, then use the handy table I created for you just below, and even colour coded (it’s a pleasure :)), and look up what percentage of your net income you’d need to save to get there. The table assumes you’re starting with a zero net worth, so if you already have some investments you’ve got a jump on most people, and can use the most simple retirement calculator in the world instead.

How much to save to get rich in a hurry

So if you want to be rich, and free to go surfing every day in 20 years’ time, all you need to do is make sure you save 44% of your net salary every month. Easy, that still leaves you with 56% of your net salary to spend every month. If you think it’s impossible, why not ask someone who earns half of what you do how they survive. It can be done. Now if that’s too slow, just save a little more. Doing that is a double edged sword, a bic razor with two blades if you like. If you save a little more, you are living on less, so the total stash you require becomes less. Plus since you’re saving more you reach this new smaller stash level even faster. So let’s hang up the tie in 10 years instead. All you need to do for that is to save two thirds of your paycheck.

Easy as pie. Now enjoy the life of leisure Mr. Gettingby, and try not to get eaten by a shark. After you’ve spent enough time catching a tan and sipping drinks from coconuts, why not give something back. I’m sure there are loads of ways your newfound free time could be used to help people around you…

As per usual, I love feedback. Even if you call me a raving loony. Leave a comment below, find me on twitter or discuss this in the forum.