Welcome to the 20s. If the last 20s were anything to go by we’ll be in for massive market gains followed by the biggest crash in history! Well either that or we’ll all start listening to Jazz and buying alcohol from the mafia. Anyway, let’s get straight into the top 9 things I learnt about money last year.

1) Some people still don’t have tax free savings accounts

Clearly I’m not doing my job well enough as a personal finance advocate and occasional blogger.

The other day I was chatting to the people in my area of the office. Amazingly, out of the 4 other people who were there at the time, not one of them had yet opened a tax free savings account.

And being my office, they can’t use the excuse that they never knew what they were because whenever anything vaguely money related is mentioned, I get on my soapbox and explain how TFSAs are the greatest invention in the world until my patent for dynamite embedded selfie sticks comes through.

It’s like having your very own tax haven, the ones politicians pay huge money for, but you can get it for free and with no risk of orange overalls. So if you’re reading this, and you still don’t have a tax free savings account, consider yourself a fool of epic proportions, and then go read why you must have one here and how to open one here.

I even opened a TFSA for my son, who now has R205 000 in it, so even if he never saves another cent in his life, he is basically guaranteed to be able to retire happily

Get one, your future self will thank you immensely.

2) People don’t want free money

Why would anyone not want free money? I just can’t understand it yet I still see people who carry cards like the Nedbank Platinum which costs R425 a month, or the Investec card that’s R535 a month. It’s madness.

In 2017 I decided that even a bank costing R0 a month was too expensive and hatched a plan to go from paying R0 to actually making a profit to bank. It worked, and in 2018 I earned R211 a month by banking strategically.

I did that by moving from FNB to Capitec, and then getting a big limit on the totally free Virgin Money credit card, and using their 55 days interest-free to pay for my monthly expenses while my salary earned 5% interest sitting in my Capitec account.

Then in 2019 an even better strategy emerged. A brand new bank run by our president’s billionaire brother in law opened (Tyme bank), and they offered completely free bank accounts with something called goal saves paying huge interest. 6% per annum in the first month the goal save is opened, increasing by 1% every month until you get to the top tier of 9%.

Now waiting 3 months to get to 9% wouldn’t do for me to deposit my salary monthly while spending on my credit card, but don’t worry because there’s a loophole…

You’re allowed 10 goal saves and you can add to them at any time, so what I do is open all 10 goal saves and put R1 into each of them. These then get to 9% interest and then when my salary arrives, I transfer it into a goalsave already on 9% and leave it there for a month before closing it so I can pay off my Virgin Money bill before I get charged any interest.

Of course after closing it, I immediately open a new one and put R1 in it so it can start building up to 9% again. I’ve also put my emergency fund into a 9% goalsave. I don’t think there’s any account in the country that pays more interest and still lets you get your money out instantly.

It’s brilliant, and in 2019 it meant that I earned R326 a month by banking! That’s an extra R3912 income for the year. Free money! Next year will be even higher as I only started this in February, and it took me 3 months to get to 9% the first time around.

There’s really no other way to say this. If banking still costs you money in 2020 you’re a complete idiot.

3) I can be a BIG spender

Not all lessons are financially positive. I did something really out of character last year. I wanted to see what would happen if I didn’t consider costs when making decisions.

It started off with the holiday my wife and I planned. We both turned 40 last year, so to celebrate we decided to take an extravagant holiday. “What’s the one thing you’ve always wanted to do but never did because it was too expensive?” was the question we asked ourselves.

For us it was hiring a catamaran and sailing around the Croatian islands. And since the boat had 4 cabins we thought, why not invite our parents along, after all both our dads are turning 70. So on top of the boat costs, I added a plane ticket for my dad. And since money wasn’t a consideration, why not throw in some spending money so he doesn’t have to worry about costs for a change. That was his birthday present for the year. Here are some photos, click next to see the rest:

We flew to Lisbon again as it's still the cheapest way to get to Europe. How do you like the restaurant location?

We flew to Lisbon again as it's still the cheapest way to get to Europe. How do you like the restaurant location?

The experiment continued after that holiday when for once I finally got the hint about a gift my wife has actually wanted for years. All it took was her dropping subtle hints for 5 years and I finally figured it out after she may have actually sent me a picture. She was really happy with it, so then I was too. Happy wife happy life.

So yes, in terms of gifts and holidays the budget was well and truly blown. If you want to see what happened to the other spending categories when I don’t care about money you can read all about it next month when I post my 2019 spending review.

4) Humans suck at risk management

I couldn’t believe I was having this conversation with someone who had a masters degree. He was telling me that he was putting his money into what he called a multi-level marketing (MLM) opportunity.

Of course I told him that it sounded exactly like a Ponzi scheme, but I wasn’t even remotely prepared for his response. Instead of trying to explain to me that it wasn’t he simply said that it probably was, but in the beginning Ponzi schemes have to pay some of the people, otherwise nobody would buy in, and he was hoping to be one of those people.

He wasn’t.

Another example is an email I got from a long term investor. He’d been investing in solid South African companies. Diversifying whenever he thought he saw a great opportunity as the experts advise of course. Until a few years ago he was convinced he was a genius because their value had gone up really consistently, until recently.

Sadly for him, his portfolio of well-diversified blue-chip companies included Discovery, Aspen, MTN, Vodacom, EOH and even Steinhoff. He’d been through a bloodbath.

And can you guess what he asked me? Which companies should I invest in next to get some quick growth and recoup my losses?

I said all of them.

As a quick reminder, picking a handful of the best performing companies is not risk management, it’s the Dunning-Kruger effect in action. Investing in all the companies on the JSE is not risk management, it’s home country bias.

Risk management is thinking of all the potential worst-case scenarios and then finding a way to still be okay with the outcome.

I invest in all the companies, so the risk of a few companies doing a Steinhoff or EOH doesn’t bother me in the least. I invest in all the countries, so the risk of a few going all Zimbabwe or Venezuela on me couldn’t bother me less.

Risk management is making sure you can sleep well at night when shit happens, because it often does. My ultimate risk management strategy is a small cheap sailboat anchored in a place where I can catch fish easily. I should be able to cut costs by at least two thirds that way which should keep me sleeping well even if we go through another great depression. Looks like a great life to me:

5) South Africa will go bankrupt

Newton’s first law states that an object in motion will stay in motion at the same speed and in the same direction unless acted upon by a force.

And without a force stopping our slide, we aren’t only flirting with disaster, we’re rounding third base and asking if disaster has any condoms. All the ratings agencies know it, the IMF knows it, our finance minister knows it, the reserve bank governor knows it, and I’m willing to bet the President knows it too.

But instead of fixing the problem (and again we’ve been given detailed instructions by the ratings agencies and the IMF on how exactly to fix it) we’re quite happy to just stand by and watch while taking out loans to plug the holes in our budget.

Now that might work for a short period, if you can pay off the loans, but we can’t so we keep taking out new loans to pay the old loans off. Have any of you ever paid off one credit card using another? How did that work out?

Since 2004, I’ve probably had around 200 trips into countries with failed or failing economies. I’ve seen what happens when a country runs out of money. The typical pattern is like this:

- Deny it’s a problem and watch while the economy slides. These crashes happen slowly at first, until all of a sudden they happen very fast.

- Crash! Time to get some money. Turn down good loans because they ask you to become more business-friendly, instead you take bad loans from shady countries.

- Run out of money to repay shady countries, so you start giving them your stuff. Minerals, trees, electricity companies, train replacement contracts etc. The truly desperate just print money, until they run out of money to pay for paper to print on.

- Ignore all the suffering, steal the future elections and what’s left in the country while the aid agencies feed the people.

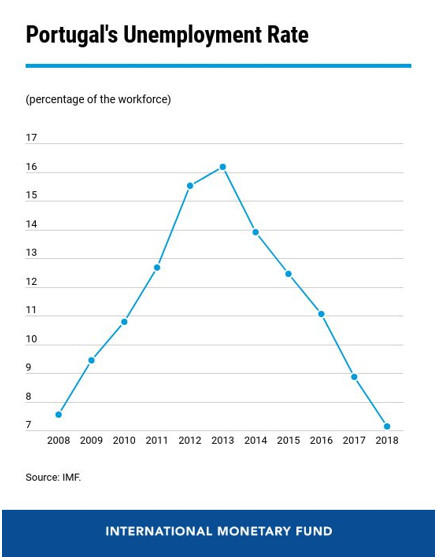

Now while we will almost certainly go bankrupt, that doesn’t have to be all bad. In very rare cases a country will take a loan from the IMF, and implement all the changes that they’ve been advised to make. In these cases the results can be fantastic. Case in point Portugal who ran out of money, but then took an IMF loan and implemented their suggestions in 2011. Here’s what happened to their unemployment rate:

It just may be that going broke and taking an IMF loan could be the best thing that happens to us. As long as we choose that path and not the other one.

6) You simply cannot beat the market

Nobody can beat the market. It’s simply impossible as I’ve said here and here, and probably a bunch more places I can’t remember now. Its something I don’t even debate people on anymore. I simply accept it as a fact, and if they don’t I just move onto a new topic while making a mental note never to ask them for any advice on anything like I do with climate change deniers, anti-vaxxers, and flat-earthers.

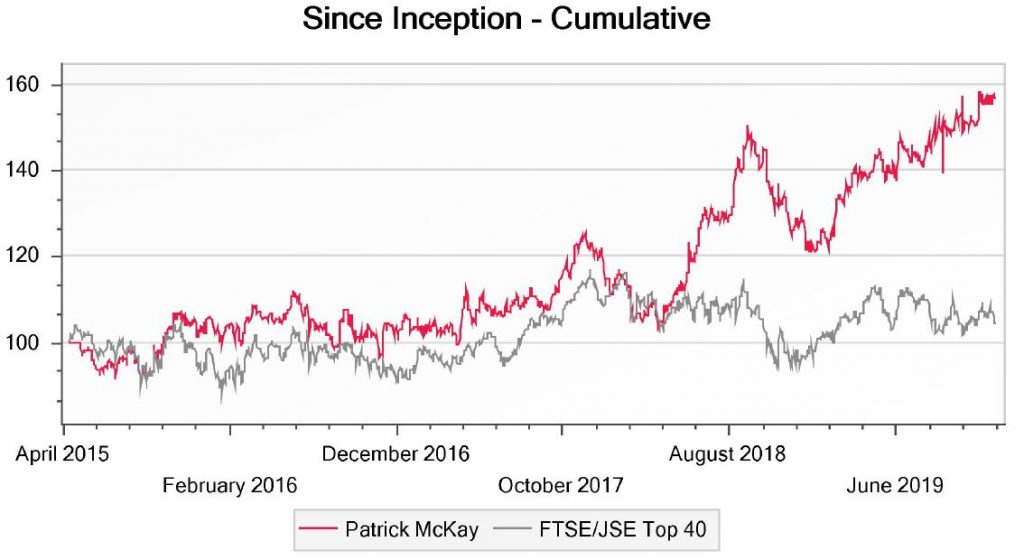

The only problem is that when I finally checked my Easy Equities statement, I saw this:

So what on earth is going on? Why have I outperformed the market by nearly 50% since I opened my tax free savings account?

Well you see I actually haven’t. What I’ve done is outperformed the local market, the JSE top 40. And that’s why I believe it’s always best to invest in the whole world, because you never know which market will be the strongest in the future, so just buy them all. This is exactly what I did, I simply bought the Satrix MSCI World ETF: STXWDM.

Outside of my TFSA I do something very similar, but I do that completely outside of South Africa as it’s cheaper that way.

7) Compound interest still surprises me

After all the money I spent without care this year I wouldn’t have expected my investment account to grow much, but that didn’t matter at all. You see once your investment account reaches FI levels, compound interest does practically all the heavy lifting for you.

In 2019, I sat back and watched as my account balance grew by more than 10 years worth of expenses without any effort on my part! Okay that’s not completely true, I had to log in and re-invest my dividends 4 times.

For years I’ve been running calculations and looking at how all the graphs shoot skyward towards the end of the investment journey, but until you get to see it happen in cold hard figures in your own account, it’s hard to actually believe. That’s why it’s so much more important to save and invest as much as you can when you’re still young. That way you’ll reach a point where you’ll be rich no matter what happens.

8) The best a man can get (ripped off)

My wife likes me with a beard, but I find it so itchy after a while that I feel like face planting onto belt sander. Fortunately for her, I like to live as low maintenance a life as possible, so I leave it as long as I can, which for me is one week.

Now I grow a beard quickly. My 4 o’clock shadow arrives at 11 am, and my beard is twice as strong as Kevlar. Seriously, I’d harvest it as a cash crop if I could stand the itch. That means I can’t do any old razor blade. I’ve tried them all, but the best for me was the Gillette Mach 3.

Trouble is they cost around R40 a blade which always just felt wrong. Some people recommend a safety razor to me before, but the only ones I could find were over R1100, and that was too much of a gamble in case it didn’t work.

Then I saw this in checkers for R27 including 5 blades:

And who would have thought, it was my best shave ever. No irritation, no ingrown hairs, and new blades are just R3 each, and don’t put any more plastic into the world, so it’s greener too.

I have to admit that I don’t actually know what I used to spend on razor blades, only that it felt like I should sell a kidney before picking any up, but now my shaving costs will be practically non-existent going forward.

9) You never know how much time you have left

It really sucks to end on such a down note, but death is a certainty. I’ve known quite a few people who passed away shortly after retiring. It was one of the reasons I wanted to make sure I could retire young and enjoy life a little.

This year was even worse. My aunt who I still considered young and in good shape passed away from cancer less than a month after she first realised anything was wrong. Nobody expected this, particularly after both her parents lived to the mid-90s

Then a short while ago one of my former classmates, and quite possibly the kindest man I’ve ever known got the flu, and then was gone a day later.

Now some people might say that we shouldn’t bother saving because life is so short, but I don’t agree. Yes it can be short, but in most cases it’s long enough that you run out of money long before you run out of time. That’s why I’m now making a few changes.

First off, I’m updating my will, my plan is to set up a trust so that I won’t be making my relatives stinking rich one day, but instead that there will be investments that send income their way should anything happen to me. Exactly how I plan to use my assets one day. I’ve seen what suddenly inheriting large sums can do to people and it’s never good.

Then I’m going to save even harder. There are so many great adventures I want to go on while I’m still young and strong, and a few of them will cost more than I spend now.

And finally, my wife and I have set a hard date for when we’re calling time on our working lives. I’m not going to put the date here, because I know I have readers in my office, and at the moment I’m seriously enjoying what I do, but the date is there and I’m really looking forward to starting those adventures!

What did you learn in 2019? Let me know in the comments.