Welcome to 2019. Happily we no longer have President Zupta running this place, but unbelievably there’s still a weird orange man in a big white house trying to build an impossible wall. Enough of the politics though, like we did in 2017, lets see what I learnt in 2018.

1) The most fun I had last year was while working…

Crazy I know, but it’s true. Of course it helps that nearly half my job has me traveling around the world to fly drones. My particular highlight was during our emergency response training in Germany, where myself and a friend were selected as the first drone operators to take part in the exercise. Basically this meant we got to go “camping” and fly drones for a 8 days non-stop while living in an artificial country filled with actors ready to give us a hard time.

During this time they did their best to make our lives difficult, which seemed to include everything that has ever gone wrong in any emergency before. There were abusive border guards, angry mobs, paperwork challenges, currency crashes, assassinations, exploding toilets and much more abuse. It was literally the most realistic exercise I’ve ever been on, and considering the amount the German government spent organising it, it’s easy to see why. It might have been the lack of sleep from nearly 20 hour workdays, but I often forgot that it wasn’t real. I totally loved it!

Aside from Germany, I also had work trips to Kenya, Niger, Malawi, Madagascar, Lesotho, Tanzania and Mozambique, plus a few inside SA. With all of that, and the new direction my career has taken, I don’t think I would have enjoyed the year nearly as much if I wasn’t working.

And that leaves me with a problem. Clearly I can’t FIRE until I think my life would be an improvement if I wasn’t working. If I could have everything I wanted, it would be to only work 50% of the time just doing the drone work and none of the more tedious aspects of my job, but sadly that’s an impossibility.

That means unless I find something more interesting to occupy my time with, or until the parts of my job I do like get overtaken by the parts I don’t I might as well keep working.

My whole world has been flipped upside down. Total mind*bleep*.

2) Earnings don’t always go up

Just so you don’t think my life is only roses, here’s a nasty thorn I got impaled with.

I’ve been working on websites and apps in my spare time for nearly 12 years now. For the last three, I’ve had pretty good advertising income from one specific site. No it’s most definitely not this one which couldn’t even pay for a bottle of water a day in ad earnings, it was a tracking app I created for Android phones.

One coding talent I believe I have is making things very simple to use. My goal with everything I build is to make it easy enough that someone non-tech savvy could use my creations without needing a manual. The tracking app was great at this, there was no requirement to register, no settings to change, not even a need to give your email address. Just install the app and get your 6 character code and you’re done.

It did really well too, a half a million or so downloads until I got an email from Google one evening in early 2018. “Dear Patrick, Your app can be used to track people (like duh, it’s called GPS tracker for Android…) and it doesn’t give them any indication that they’re being tracked. Sorry but we’re banning it from the app store. Feel free to relaunch it when you meet all our requirements, but that one is gone forever.” I appealed and lost, understandably.

Then of course I poured through the requirements, found out that it was missing an icon with a message that lived on the screen informing people that tracking was active. I added it and relaunched, but sadly I had to start from the bottom of the search rankings. That means I went from around 500 installs a day to 100, with a similar loss of income.

Then about 8 months later I got another email from Google. “Dear Patrick, Your app can be used to track people and it doesn’t give them any indication that they’re being tracked (now completely wrong). Sorry but we’re banning it from the app store. Feel free to relaunch it when you meet all our requirements, but that one is gone forever.”

This time I was really confused, so I appealed again, this time quoting their requirements and showing how I complied on every level and lost again. Google work on a 3 strikes and you’re out system, so relaunching again would risk killing off my developer account completely, and it’s not worth the risk.

At it’s best, that app paid for two thirds of my living expenses.

To rub some salt into the wounds, my annual salary at work was also adjusted. Our office does reviews of what the market related salaries are for each level of staff, and then use that to allocate increases.

Two years ago it was 3.4%, below inflation. 🙁 Last year 3.1%, again below inflation. Would you like to guess what it was this year? No you’re wrong, it was -3.3%. Yes this year I got a pay decrease even though 2018 was one of my most successful years in terms of achievements.

They don’t actually implement negative increases, but if by some miracle next year we actually get an inflation based increase of 6%, I’ll only actually get the remaining 2.7%.

It was a good lesson to learn though. If, like so many South Africans, I’d used every bit of income that came into my account to buy big cars and expensive houses I’d be in serious trouble. Fortunately for me it was surplus money, it’ll affect how much I can save, but it won’t have me at risk of losing my house or having my car repossessed.

Always live below your means, just in case you end up with less means!

3) Don’t just weather the storm, dance in the rain

If you were following any of the mainstream finance news or the experts on Twitter in December, from the panic all around you’d swear that we were on the cusp of the second great depression instead of the first bear market in 10 years. It wasn’t anywhere near as bad as made out to be, even though at it’s lowest point I’d “lost” 8 years worth of living expenses, yes EIGHT!

Was I upset about it? Not even slightly. I was grinning wider and wider with every drop. You see I have a system of working out when to panic and when not to. All you need to do is ask yourself these two questions:

- Am I diversified globally? In other words it’s not your choice of companies or a single economy you’ve put all your eggs into but just the general global stock market that’s doing it’s thing.

- Am I still working and putting money into the market?

If you answered yes both times, then you have absolutely nothing to worry about. It’s not a crash or a correction, it’s a major discount. Like black Friday for shares!

If you’re not working then you need to hope your withdrawal rates are low enough and that you have a cash buffer to sail through this. Remember, the 4% rule is there for the worst years, and survived even the nearly 90% crash of 1929.

Just keep putting your money into the market and ignore all the noise that happens every now and again. The stock market is and likely always will be the greatest wealth generator we’ll ever see.

The global market can stutter, go through corrections, crashes and total meltdowns but it will always recover and go on to make record highs. Repeatedly. The same can’t be said for a single share or a single economy.

Just keep buying, and remember last years lesson on diversification…

4) Sometimes I’m wrong

You might not believe this is possible, but it does happen, my wife can vouch for this. For years now I’ve been saying that you’re financially better off if you invest internationally. No that’s not what I’m wrong about, but it’s the fund domicile (like the fund’s home base) I may have made a mistake on.

This is a long lesson, so I’ll give a quick summary to those who aren’t interested in tax law: I was wrong, you can’t claim dividend tax credits from Ireland if they don’t appear in a document from your broker. Oh and SARS sucks more than Justin Bieber on repeat.

Most of you can now skip to the next point, but if your spouse has ever asked you to stop talking finance in bed then you’ll probably find the long version interesting…

Like most of the smart non-American world, I put all my money into the Irish Vanguard all world index, VWRD, rather the the US Vanguard all world index, VT. This is because all the calculations showed that when you take everything into account you pay less in taxes and fees when investing through Ireland than you do through the US, and once you die you won’t have to give over huge sums of money to that orange man in the form of estate duties.

Except that’s not actually the case, as our wonderful SARS team proved when they decided to review my taxes last year.

You see with the Irish fund, dividend taxes are taken off internally (and almost invisibly) at around 11.8% and then the net dividend is paid to you. With the US fund you get paid the gross dividend, and then the US withholds 15%.

The catch is that in the first case, the 11.8% is not explicitly shown, rather the Irish annual report shows the total the fund received in dividends ($28m last year), and the total paid in foreign withholding taxes ($3.3m last year), which works out to 11.8%.

I then work backwards to figure out what my gross dividend was which I put on the tax form, and then put my portion of the taxes paid into the tax credit field.

Well this year they asked for my documents, so I supplied the report page where it lists the numbers above, and the excel sheet where I worked out what the gross dividends would have been and the taxes relevant to my dividends.

After two months of no reply I got impatient and asked SARS to hurry up. This may have been a mistake, as the next day they simply threw out any reference to my tax credits and sent me a bill.

Now I still believe I’m right, but I’m not yet quite sure how to fight it. My case is that in some instances SARS does take evidence from annual reports into account. For example, if you were to invest in the Irish iShares MSCI world ETF, IWDA, you’d find that it doesn’t actually pay any dividends, it builds them back into the price of the share. This is called a total return index.

What SARS makes you do in that case is using all the reports available to work out what dividend would have been paid to you if it wasn’t re-invested, and then charges you dividends tax on that.

So basically they take your calculations into account when it makes you pay more tax, but not when it means you could pay less? I’m out of my league with tax laws, so if there’s an expert reading who wants to give me a hand I’d be very keen to listen.

One area where Ireland definitely has the tax upper hand though, is they don’t charge any estate duty on funds, while with the US it could go up to 40%. So at least I’m definitely still right for after you die 🙂

My solution for now is to start putting money into the US based Vanguard all world (VT), and to remember to move most of it before I die 😉

Paying for expert advise could have saved me some money here.

5) Sometimes I’m right

Last year my second point was about my great plan to go from paying zero in banking fees, to actually getting paid to bank. The plan was to up my credit limit on my completely free Virgin Money credit card to cover my monthly expenses, and then to spend their money interest free while my cash earns 5.4% interest in my cheap to run Capitec bank account.

I was estimating I’d gain R1800 a year, but yet again I was wrong!!!

Last year my bank charges totaled just R433 for the whole year, but my interest received was a significant R2963 for the year. That means that I made a profit of R2530 just for banking smartly! That’s an extra R211 a month, which I think is brilliant.

And all I had to do was send one email to Virgin to increase my limits, and then make sure I pay them every month. Money for nothing if you ask me.

On a similar topic, David Shapiro the 702 market commentor recently posted this tweet:

Now before I was with Capitec, I was with FNB, but before that I was with Standard Bank, and at that time I was spending +- R200 a month in bank charges and account fees. Of course there wasn’t a Capitec or Virgin money around at that time, but let’s work out what a pen like that could cost me if I never optimised my banking.

With Capitec/Virgin there’s a profit of R211, with Standard there’s a loss of R200, so the total gain with Capitec/Virgin is R411 a month. Now let’s go and invest that at market average returns for 50 years: Calculation here.

Yes that’s a cool inflation adjusted R3.4 million rand, maybe you wouldn’t have to be working today after all David. But hey, if the pen was the 8 carat diamond and ruby encrusted Montblanc Prince Rainier III Limited Edition 81 you’d actually break even. In that case, please don’t lose it!

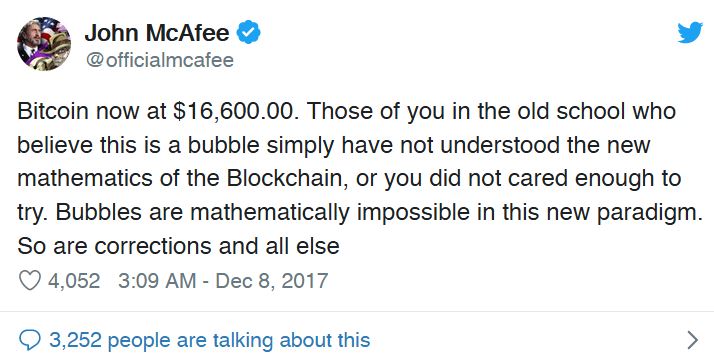

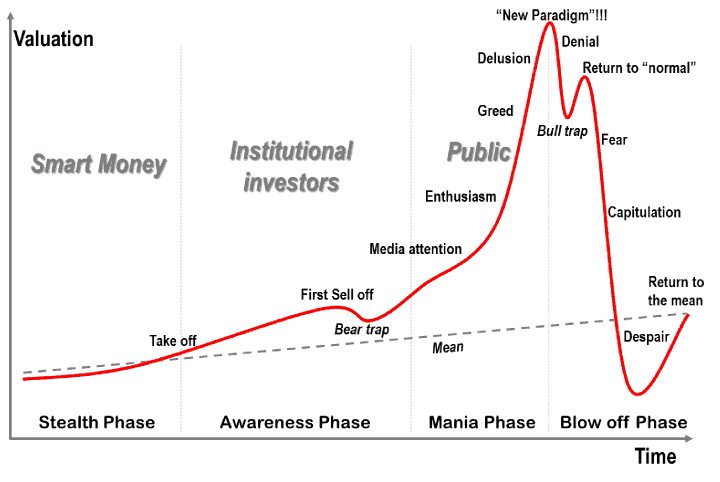

6) If it looks like a bubble, and acts like a bubble…

There was a debate in the beginning of 2018 about whether we should add Bitcoin to the challenge. A ton of people said nooo it’ll destroy the competition because Bitcoin will always be on top. I had a different theory, I thought it would end right at the bottom. And look there, another time I was right.

For future knowledge, here’s the pattern of a bubble. The minute someone mentions new paradigm SELL!

7) South Africans sure do love giant cars

I ended the year with a roadtrip to Cape town, around some of the garden route, and then home after spending a couple of days in Nieu Bethesda, which is a really cool little town if you haven’t been there yet.

One thing that struck me on the roads, was just how many giant SUVs and expensive double cab bakkie’s there were doing the trip. They were almost the default vehicle. With many of those costing R9+/km a roadtrip to Cape Town and back can easily cost R27 000, and that’s without any traveling while you’re there!

Do the calculation on the costs before you choose a transport method.

8) But even old cars can sometimes be expensive

I drive an old Nissan Almera, it’s been super reliable, but it’s 15 years old so things are going to go wrong. Last year while driving home I heard a massive explosion coming from the front of my car. I thought a tyre had burst so I stopped quickly to check when I saw steam rising rapidly from my bonnet. The entire top of my radiator had literally blown itself to pieces.

The next day I called the Nissan dealer where I take my car for services. The quote for the radiator to be replaced was over R11 000. I tried to explain that I was only replacing the radiator and not keeping the radiator and attaching a new car to it. He didn’t laugh.

I made a few more calls to radiator specialists and their quotes were all around R2k. The one guy at Silverton radiators had seen this quite a few times before. Apparently it’s common on old Almeras for the thermostat to seize up, and that just replacing the radiator would lead to another burst. He said he’d source me a new thermostat, replace that and the radiator all for just under R2k and it would be guaranteed for a year. He got my business.

If something sounds outrageous start looking for more quotes.

What about the rest of you, what did you learn in 2018?