Well not exactly you of course, you’ll be dead. And not in terms of funeral costs, church costs, hall hire, catering, burial site, flowers, tombstones, etc, you already know about those. These are different. Do you remember the time SARS said they were raising taxes, and you replied “Over my dead body”. Well yeah, they were listening, and now have plans to take massive amounts of money away from your kids one day.

It’s called estate duty, some countries have it like us, Japan, the Brits, and many others, but there are also a whole bunch of countries who don’t have this tax. Canada, Australia, Portugal and Sweden for example don’t charge you anything for dying.

As I pointed out in point four of my 2018 lessons learnt post, America is a bit of a weird one. They charge both locals and foreigners estate tax, and at a really high rate of 40%. Most Americans don’t mind though, because you don’t pay it on the first $11 million!

Sadly for non-Americans (they call us aliens, really) you pay it from the time you have over $60 thousand in the country, which is why I keep most of my investments in Ireland where I won’t need to pay this to enter the pearly gates.

So how does it work for South Africans?

Our estate duty starts at R3.5 million. Anything over that is taxed at 20%. If you’re one of the big savers who read my blog and one day have over R30 million, you’re going to pay 25% on all of that.

Personally, I’m not too concerned by that. I think my family would be just fine on 80% of what I leave them, and I’ll probably live out my days in Portugal anyway, so I won’t need to pay anything, but for a lot of people who need to potentially live a very long time on what you leave behind it makes a huge difference.

BUT, death taxes aren’t the only expense you need to worry about. If you let your bank do your will for free like they always offer to do, you’re a hugely stupid person.

What the banks hide in the fine print, is that they take the absolute maximum fee for being the executor, 4.025% after VAT is included. That is a monstrous amount of money for the amount of work required.

If you’re worth R10 mil when you die it means they’re going to take over four hundred thousand rand! If you’re wealthy enough to die with R25 million say goodbye to R1 million for a job that your relatives could do themselves, or with the help of a fixed fee lawyer.

And to make things more interesting ridiculous they take the money from your gross estate, not your net estate. So if you have a R6 million house, but you still owe R3 million on it, you’ll pay executors fees on the full R6 million.

As you can see, your bank doing your will for free is quite possibly the most expensive piece of paperwork you’ll ever sign.

If your estate is simple your family can handle it by themselves, but if not they’re free to appoint anyone to help. They can get a few quotes and agree on the fees upfront rather than paying a massive percentage-based fee.

If you’re about ready to tear your hair out you still need to hold of for a bit, because there’s yet another fee. That R6 million house you left to relatives will need to be transferred into their name. Welcome to some transfer duties. On a R6 million house that works out to over R500 000. On a more modest R2 million house it would be nearly R80 000.

So what can we do about all this graveside robbery?

Here are a few options, some quick and easy, some a little more complicated:

- Easy: Don’t let the bank or

investment housespolicy salesman be your executor - Easy: Leave as much to your spouse as possible – In SA, any assets left to a spouse won’t have to pay estate duty until the spouse passes away

- Complicated: Move to a country that has no estate duty before you die.

- Complicated: Set up a trust and put your assets into it before you die. Trusts can own things, but they don’t die, so you wouldn’t need to pay estate duty on your death

And there, in those four points, I’ve just saved you hundreds of thousands, if not millions of rand.

You’re welcome.

And now onto the fun scary bit. Let’s go plug in some numbers into my stupidly simple Death Cost calculator to see how much money your family will lose after you kick the bucket.

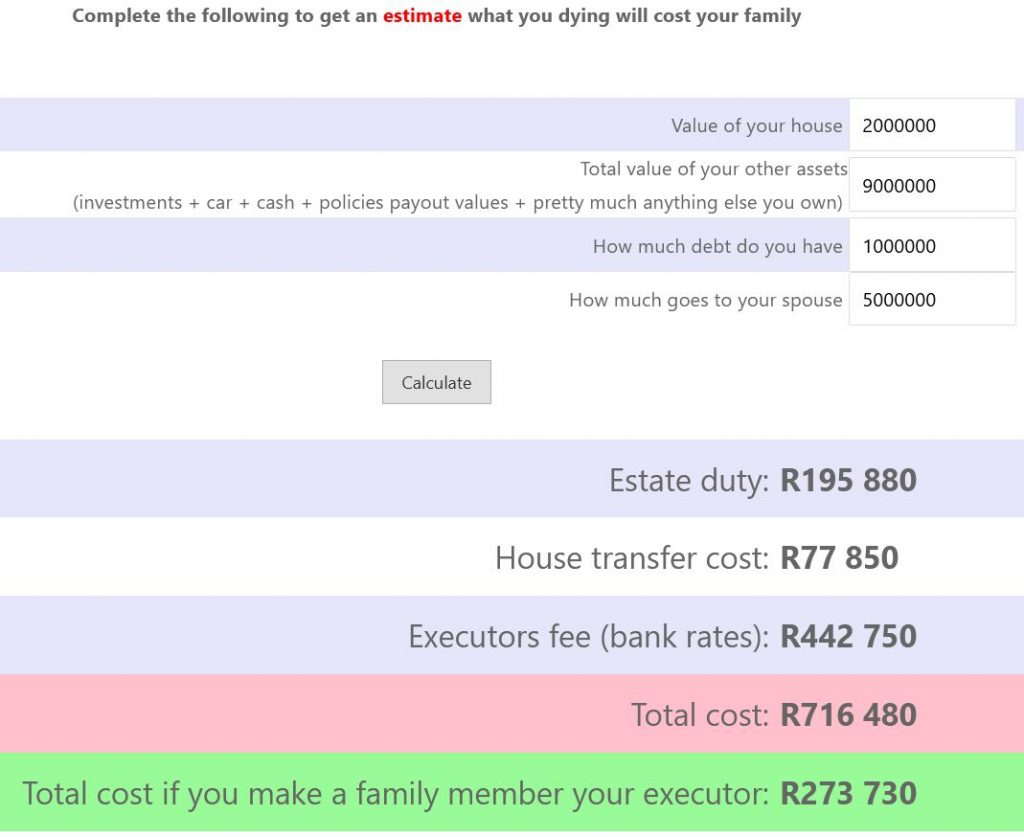

Peter owns a R2 million house, with R1 million left on the bond. Apart from that, he has R8 million in investments, a R500 000 car and around R500 000 in cash. What will it cost his family if his base jumping rig fails this weekend:

As you can see it will cost him around R700 000 if he leaves his bank as the executor of his will. If he makes a family member executor it’ll save him R440 000. Make the smart move Peter, and maybe give up base jumping 🙂

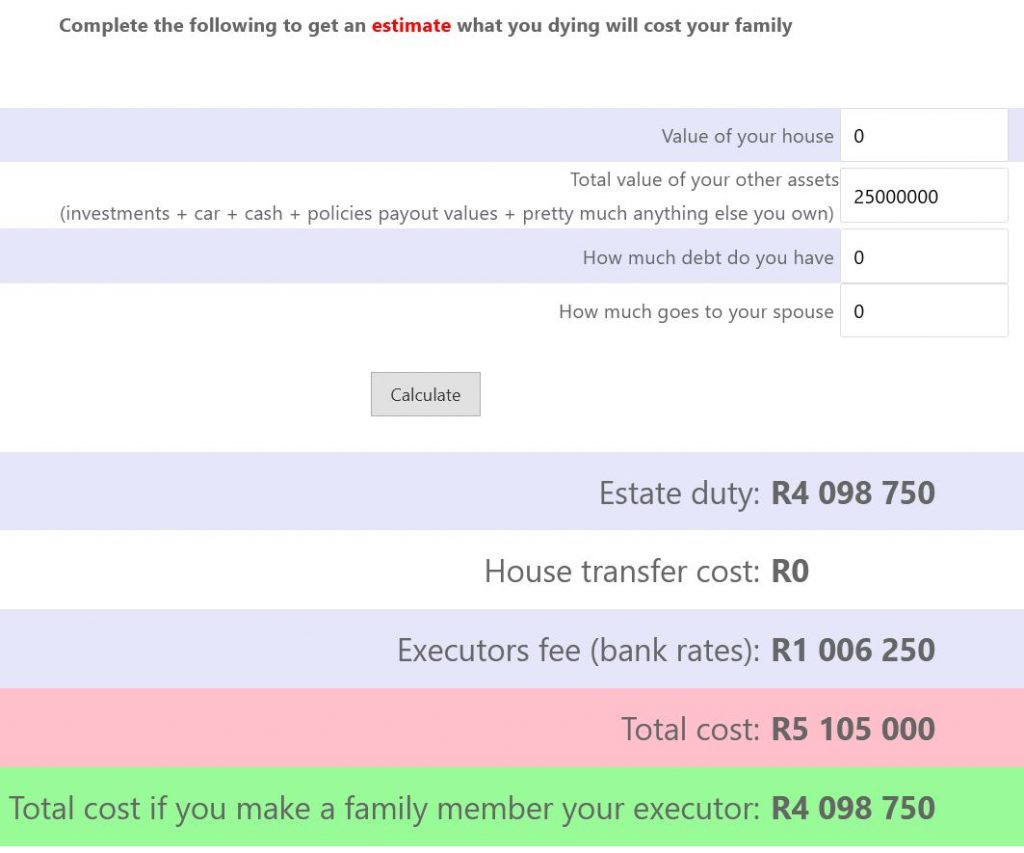

Let’s do another. Penelope is very smart, she rents a house and puts everything else into ETFs. As such she’s built up a sizeable investment account of R25 million. She has no debt, and left her husband years ago for a younger toyboy. All of her assets will be left to her only child:

If you were Penelope’s child you’d really want to tell her to steer very clear of letting a bank/investment house be the executor of her will. As it’s simply one investment account, it’ll be really simple to deal with. Paying the bank over R1 million rand just to transfer a single brokerage account into her child’s name is purely ridiculous.

One last major warning. If you don’t have a will you’re an idiot. I was that idiot until a few years back, then I found out that without a will, my investments would be sold off and the remains split between my wife and kid equally.

So far so good right? Not quite. Without a will the government is going to take my child’s portion and then put it into something called the Gaurdian’s fund, and then the child will get it when they’re 18 after filling in a few dozen forms and getting certified copies of every document you’ve ever received.

As you can see that might be a problem when it comes to paying school fees, but for that you need to fill in 3 forms, provide receipts for every expense and again certified copies of enough forms to keep you in a home affairs queue for 17 months.

If that’s not scary enough think about this. Without a will, you’ll be letting the same people who managed SAA and ESKOM so well look after your kids inheritance. Don’t be THAT person!